Israel’s sovereign credit rating on Tuesday was lowered by credit rating agency Morgan Stanley, and Moody's warned of a "significant risk" that political and social tensions will lead to "negative consequences for Israel's economy and security situation," following the Knesset’s vote to pass the first law of its controversial judicial reform on Monday.

Morgan Stanley updated Israel’s sovereign credit to a "dislike stance," noting that the government has reaffirmed the trajectory of its economy in a direction that is likely to scare off investors.

"We see increased uncertainty about the economic outlook in the coming months and risks becoming skewed to our adverse scenario,” the agency said. “Markets are now likely to extrapolate the future policy path and we move Israel sovereign credit to a 'dislike stance.’”

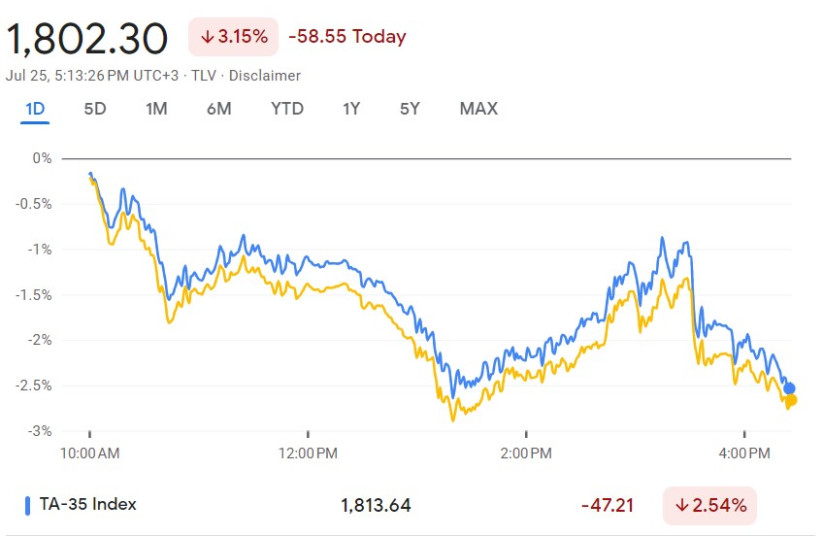

They added that recent events indicate "ongoing uncertainty" in Israel and that the shekel is likely to continue depreciating alongside the Tel Aviv Stock Market, which has lost nearly 10% since November of last year.

Shoveling more problems onto the pile

Moody's warned that there is "a significant risk that political and social tensions over the [judicial reform] will continue, with negative consequences for Israel's economy and security situation."

The credit rating agency warned that it believes that "the wide-ranging nature of the government's proposals could materially weaken the judiciary's independence and disrupt effective checks and balances between the various branches of government, which are important aspects of strong institutions."

The agency added that "the executive and legislative institutions have become less predictable and more willing to create significant risks to economic and social stability."

Moody’s announcement was made outside of its standard schedule for rating updates, which would have seen the next update in October. Given the outlook of Morgan Stanley and prior statements from Moody’s, the latter can likely be expected to demote Israel’s rating as well.

In April, the agency affirmed Israel’s sovereign credit rating at "A1" but downgraded the outlook on the Israeli government's credit ratings to "stable" from its prior status as "positive." Moody’s cited “a weakening of institutional strength and policy predictability” and “a deterioration of Israel's governance” as its primary concerns for Israel’s economy.

Netanyahu, Smotrich dismiss Moody's announcement as a 'momentary reaction'

Prime Minister Benjamin Netanyahu and Finance Minister Bezalel Smotrich dismissed the announcement set to be published by Moody's on Tuesday afternoon, stating "This is a momentary reaction, when the dust settles it will become clear that Israel's economy is very strong."

"Israel's economy is based on solid foundations and will continue to grow under an experienced leadership that leads a responsible economic policy."

For months, hundreds of economists, experts, and executives throughout Israel and around the world have warned against the current government’s plan for judicial reform, claiming that it will lead to a sharp decline in foreign investment due to a lack of economic stability brought about by the weakened legal system.

Recent credit rating downgrades are only the latest signs of damage to the country’s economy. According to a report from Start-Up Nation Central published on Sunday, 68% of start-ups have already initiated steps such as withdrawing cash reserves, relocating their headquarters outside of Israel, moving employees abroad, and conducting layoffs in response to the judicial reform’s impending effects on the economy.

“Whatever your political views about it, what's happening now in the country reflects big time on the business community. Now, doing business with Israel is a little bit more complicated, more risky, and that's largely affected Israel’s overseas income,” Aman Group CEO Ben Pasternak told The Jerusalem Post. “Now, uncertainty is very large around the world as it is, but in Israel it’s even higher… Uncertainty kills business.”